|

Feb 12 2009, 10:01 AM Feb 12 2009, 10:01 AM

Kiriman

#1

|

|

|

Bukan Eksekutif  Kumpulan: Member Rasmi Kiriman: 12 Sertai: 12-February 09 No. Ahli: 689 |

Salam

Saya adalah PerwaRis di Carigold dan Putera.com dan amirul_nazri di forum cari. Tujuan saya open 1 new thread adalah kerana my approach dlm handling investment pelabur mungkin ada sedkit beza dpd apa yg korang biasa dengar dan baca dpd UTC lain Unit Trust is bukan semata2 ekuity fund Unit Trust juga ada fixed income fund (bond dan money market) yg offer capital preservation dan bg steadier income espescially during volatile environment. My point is, for those yg plan to buy investment in moderate-huge amount espescially by $$, pelabur should consider certain portion to park into fixed income fund, espescially bond. Fixed income funds are usually invested in bonds and interest-bearing instruments and are generally steadier and offer capital preservation. The expected return for a bond fund should be two to three percentage points above the fixed deposit rate. The risks are significantly lower with bond funds when compared with equity funds and you should consider them as an alternative to your fixed deposits. Everyone should invest into bond fund kerana bond fund bg some liquidity in case pelabur need cash on urgent basis. Unit Trust bukan hanya semata-mata dollar cost averaging (monthly topup) Practise dollar cost averaging, which allows pelabur to average down by buying more units when prices are low and less when they are high. If pelabur had invested during the market high in 1997 and practised dollar cost averaging, mereka would probably be in the black by now. However, DCA it is not the only way to maximize return dan minimumkan loss... Unit Trust have switching, as a tool to maximize return dan reduce loss also. Sebelum itu, pelabur kena faham ttg one [1] very2 common trend iaitu apabila ekuity fund turun, maka bond akan naik..ekuity fund naik, bond akan turun. The strategy is, do switching as on when necessary based on index market movement. In general, when pelaburan ada generate untung, switch all your capital + unrealized profit from ekuity to bond fund (to lock profit), when market drop, re-switch balik to ekuity fund, di mana ur initial investment then would be capital + profit. Kerja switching nie sebnrnya agent yg kena buat but it your responsibility to remind them as well. Please alert them, get the update on regular basis.The cost involved pula would be minimum as RM 25 (switching fee) and service charge. But fyi, service charge is nothing to loose as the return generated from bond helps to compensate the switching fee. For mutual gold (investment > 100K)...switching is free. Saya stongly suggest kepada bakal pelabur agar buat asset allocation juga spt di bawah (sumber dpd Public Mutual dan Fundsupermart) Conservative Bond 50% Equity 50% Rate of Return: 5.6% Moderate Bond 45% Equit 55% Rate of Return: 6.6% Agressive Bond 30% Equity 70% Rate of Return: 7.4% Assuming annualized return of Bond = 6% & Equity = 9%...Annualized return is Effective rate of return, minus tax dan inflation. saya mengalukan2 feedback ttg post saya nie. Boleh kita berbincang sbb maybe agent lain tak sependapat ngan saya..ttg sesapa nak tahu dgn jelas ttg camna saya gunapakai switching utk dapatkan keuntungan semaksima yg boleh dan reduce loss seminimum yg mungkin,bole email saya di nazri.amirul@gmail.com.insyaallah saya akan show sample akaun clients saya APa yg saya quote di atas is based on my 3 1/2 years experience jd agent. Difference consultant, different style, difference return..

-------------------- Agency Manager, Public Mutual

019-6928364 @ nazri.amirul@gmail.com ym; amirul.nazri |

|

|

|

Mar 5 2009, 11:40 PM

Kiriman

#2

|

|

Eksekutif Kumpulan: Moderator Kiriman: 742 Sertai: 2-June 08 Daripada: Saujana Putra No. Ahli: 4 |

saya ada invest ke unit trust public mutual ni drp pakej skim KWSP, ambik Public Islamic Dividen Funds.. sakng market tgh murah maka tgh tambah investment setiap 3 bulan, tp tgk market jugak sbb nak beli pada harga yg betul2 murah.. saya amat rekemen sape2 yg nak invest for long term guna skim KWSP ni.. sbb kalo simpan duit dlm KWSP pon bape sen sgt dpt dividen, baik kita laburkan utk lipat ganda kan dana KWSP kita ni demi hari tua nanti..

-------------------- matg.net

My Focal 2.0 |

|

|

|

|

Mar 6 2009, 06:16 PM

Kiriman

#3

|

|

|

Bukan Eksekutif Kumpulan: Member Rasmi Kiriman: 12 Sertai: 12-February 09 No. Ahli: 689 |

QUOTE (mat.g @ Mar 5 2009, 11:40 PM)  saya ada invest ke unit trust public mutual ni drp pakej skim KWSP, ambik Public Islamic Dividen Funds.. sakng market tgh murah maka tgh tambah investment setiap 3 bulan, tp tgk market jugak sbb nak beli pada harga yg betul2 murah.. saya amat rekemen sape2 yg nak invest for long term guna skim KWSP ni.. sbb kalo simpan duit dlm KWSP pon bape sen sgt dpt dividen, baik kita laburkan utk lipat ganda kan dana KWSP kita ni demi hari tua nanti.. u had make the right move bro... those yg buy investment during economic woes now, akan dpt return yg bagus bila market dah recover nanti..dan mereka akan bersyukur. -------------------- Agency Manager, Public Mutual

019-6928364 @ nazri.amirul@gmail.com ym; amirul.nazri |

|

|

|

|

Mar 6 2009, 09:36 PM

Kiriman

#4

|

|

Eksekutif Junior Kumpulan: Moderator Kiriman: 392 Sertai: 8-October 08 Daripada: India No. Ahli: 103 |

benarkah Unit trust mengamalkan breakthru system ?

--------------------  |

|

|

|

|

Mar 7 2009, 12:30 AM

Kiriman

#5

|

|

|

Bukan Eksekutif Kumpulan: Member Rasmi Kiriman: 12 Sertai: 12-February 09 No. Ahli: 689 |

QUOTE (Padaiyappa @ Mar 6 2009, 09:36 PM) benarkah Unit trust mengamalkan breakthru system ? not realy...depends on the style adopted by consultants dan taste pelabur.

-------------------- Agency Manager, Public Mutual

019-6928364 @ nazri.amirul@gmail.com ym; amirul.nazri |

|

|

|

|

Mar 8 2009, 09:29 PM

Kiriman

#6

|

|

|

Bukan Eksekutif Kumpulan: Member Rasmi Kiriman: 12 Sertai: 12-February 09 No. Ahli: 689 |

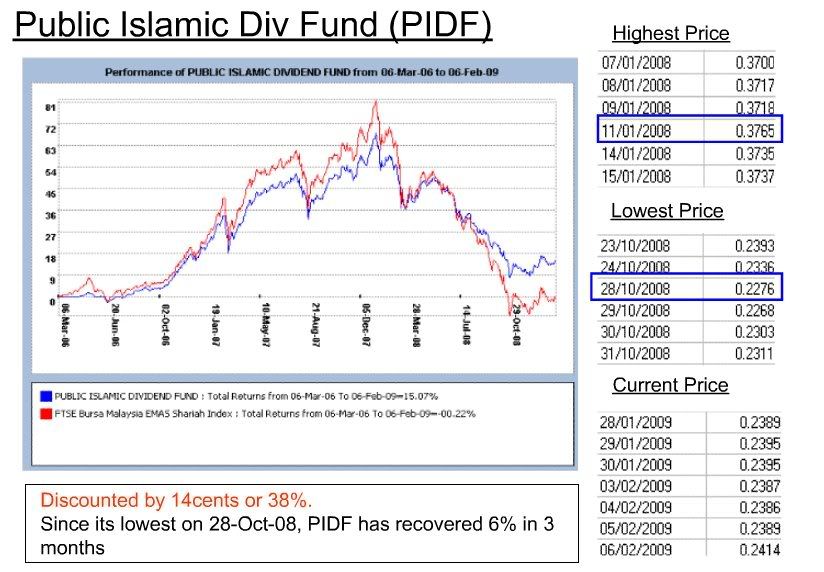

kindly take a look on discounted prices of 2 popular funds in Public Mutual

Lets buy low....   -------------------- Agency Manager, Public Mutual

019-6928364 @ nazri.amirul@gmail.com ym; amirul.nazri |

|

|

|

|

Mar 12 2009, 12:23 PM

Kiriman

#7

|

|

|

Bukan Eksekutif Kumpulan: Member Rasmi Kiriman: 12 Sertai: 12-February 09 No. Ahli: 689 |

KLCI index now move on to new low...

lets define this oppurtinities..buy low now, from medium to long term, the potential of return is huge...

-------------------- Agency Manager, Public Mutual

019-6928364 @ nazri.amirul@gmail.com ym; amirul.nazri |

|

|

|

|

Mar 12 2009, 12:44 PM

Kiriman

#8

|

|

|

Eksekutif Kumpulan: Moderator Kiriman: 742 Sertai: 2-June 08 Daripada: Saujana Putra No. Ahli: 4 |

QUOTE (PerWaris @ Mar 12 2009, 12:23 PM) KLCI index now move on to new low... lets define this oppurtinities..buy low now, from medium to long term, the potential of return is huge... bro.. you the expert, so which Fund did you recommended.. now i'm only buying Public Islamic Dividend (PIDF) -------------------- matg.net

My Focal 2.0 |

|

|

|

|

Mar 12 2009, 06:46 PM

Kiriman

#9

|

|

|

Bukan Eksekutif Kumpulan: Member Rasmi Kiriman: 12 Sertai: 12-February 09 No. Ahli: 689 |

QUOTE (mat.g @ Mar 12 2009, 12:44 PM) bro.. you the expert, so which Fund did you recommended.. now i'm only buying Public Islamic Dividend (PIDF) Public islamic dividend fund bagus gak bro..cuma oleh sebb dia belum 3 years, maka belom entitle reward dpd edge & lipper aku highly recommend ko amik Public Islamic Equity Fund (PIEF)..fund nie dpt high score mark dan " 5 Star " dpd Edge & Lipper dan Morning Star. Fund nie agresif but client2 aku yg buy during November 2008 dan December 2008, diorang sempat gained 2%-3% untung pada February 2009 (which now aku dah switch temporarily to bond fund utk lock profit). Mat.g meh invest bawah aku plak..aku actively play switching utk maximize return dan reduce possible losses. Bg aku, unit trust bukan setakat peram2 ajer...kena manage Difference consultant, could come out with different return. -------------------- Agency Manager, Public Mutual

019-6928364 @ nazri.amirul@gmail.com ym; amirul.nazri |

|

|

|

|

Mar 13 2009, 05:44 PM

Kiriman

#10

|

|

|

Bukan Eksekutif Kumpulan: Member Rasmi Kiriman: 12 Sertai: 12-February 09 No. Ahli: 689 |

sesapa yg nak melabur through aku.just for info, aku actively managed akaun by switching (terhad utk mereka yg invest more than 5K, 1K ajer, buat DCA lagi baik)

sape yg join group aku..aku akan ajar technical2 knowledge ttg UT, lebih yg korg bley dpt dpd di forum dan kelas2 training.. camna nak buat sales...aku bg praktikal training sekali, company bagi dan agency aku skali sesapa nk jumpa aku, bley mai booth aku di matta Fair di PWTC Ahad nie..9am - 3pm

-------------------- Agency Manager, Public Mutual

019-6928364 @ nazri.amirul@gmail.com ym; amirul.nazri |

|

|

|

|

Mar 18 2009, 02:27 PM

Kiriman

#11

|

|

|

Bukan Eksekutif Kumpulan: Member Rasmi Kiriman: 12 Sertai: 12-February 09 No. Ahli: 689 |

Nie aku copy & paste bulat2 dpd 1 artikel yg di post di Bicara jutawan.com.. Backdated 2007 but still useful as peringatan..

Miskin selepas pencen -- Dengan purata caruman RM114,000 pesara belanja RM475 sebulan KUALA LUMPUR 18 Okt. Kumpulan Wang Simpanan Pekerja (KWSP) mempunyai caruman terkumpul berjumlah RM224 bilion sehingga Disember 2006 namun secara purata simpanan seorang pencarumnya yang mencapai usia 55 tahun cuma RM114,000. Dengan simpanan sebanyak itu, seseorang pencarum KWSP yang bersara hanya mampu membelanjakan RM475 setiap bulan bagi membolehkannya menampung hidup sehingga usia 75 tahun. Perbelanjaan RM475 sebulan akan meletakkan pesara berkenaan dalam kategori golongan berpendapatan di bawah paras kemiskinan. Pendapatan orang yang dikategorikan miskin di Semenanjung kini ditetapkan RM530 sebulan, Sarawak (RM585) dan Sabah (RM685). Pengurus Kanan Perhubungan Awam KWSP, Nik Affendi Jaafar memberitahu, pada masa ini purata caruman terkumpul kira-kira 47,500 pencarum KWSP yang akan genap umur 55 tahun pada tahun ini ialah RM114,000. Jumlah simpanan ini tidak mencukupi berdasarkan anggaran mereka akan menggunakan wang itu selama 20 tahun berikutan jangka hayat yang semakin panjang serta kos sara hidup yang terus meningkat, katanya kepada Utusan Malaysia dalam satu temu bual di pejabatnya di sini. KWSP mempunyai kira-kira 11 juta pencarum dengan 47,500 orang akan mencapai umur bersara pada tahun ini. Menurut Nik Affendi, bagi memastikan pencarum KWSP dapat bersara dengan selesa, setiap ahli dana pencen itu perlu mengubah sikap mereka yang berharap sepenuhnya kepada caruman KWSP untuk menampung hidup selepas bersara. Caruman KWSP setiap bulan hanya melibatkan 11 peratus daripada gaji mereka, jadi masih terdapat 89 peratus pendapatan pencarum yang boleh digunakan untuk membuat pelaburan yang akan menghasilkan pulangan tetap pada usia tua, ujarnya. Nik Affendi menasihatkan para pencarum supaya berhemah ketika membuat pengeluaran awal sebelum persaraan membabitkan pelbagai skim yang telah disediakan oleh KWSP termasuk pengeluaran rumah, pendidikan dan kesihatan. Jika mereka mempunyai sumber lain, simpanan KWSP harus dijadikan sebagai pilihan terakhir, tegasnya. Ditanya mengenai langkah-langkah yang telah diambil bagi memastikan simpanan persaraan setiap ahli bertambah, katanya, struktur akaun ahli KWSP telah disusun semula daripada tiga akaun kepada dua mulai 2 Januari lalu. Sebelum ini, sebanyak 60 peratus daripada caruman bulanan ahli dikreditkan ke dalam Akaun I manakala 30 peratus ke dalam Akaun II dan 10 peratus ke dalam Akaun III. Penstrukturan itu menyebabkan Akaun I yang khusus untuk tujuan persaraan dan hanya boleh dikeluarkan setelah pencarum mencapai usia 55 tahun ditingkatkan sebanyak 10 peratus kepada 70 peratus. Selaras dengan perubahan itu, ujar Nik Affendi, pengeluaran kesihatan yang sebelum ini hanya boleh dibuat daripada Akaun III kini boleh dikeluarkan daripada Akaun II. Wang dalam Akaun II yang melibatkan 30 peratus caruman ahli juga boleh dikeluarkan untuk pembiayaan perumahan, kesihatan, pendidikan dan apabila cukup umur 50 tahun. Majority neglect retirement plans Friday March 14, 2008. The Star Online KUALA LUMPUR: More than half of Malaysian workers have not prepared for retirement while those who have, only started planning after age 40, according to a survey. The average age working Malaysians began preparing for retirement was 41, while retirees said they did so at 47. Thats way too late. It doesnt give them enough time to build their retirement fund, Axa Affin Life Insurance Bhd branding and communications head Cheah Leng Sooi said in announcing the findings of the AXA Retirement Scope 2008. In the survey carried out by research house Synovate, 313 working people aged 25 and above and 319 retirees aged below 75 in urban areas were interviewed over the telephone. The survey, part of a global study conducted in 26 countries and involving 18,000 respondents, was undertaken for the first time in Malaysia, from July 23 to Aug 27 last year. Among those who had planned for retirement, most began after they married, had children, or fell into financial difficulties or had health problems, Cheah said. Their sources of retirement income included life insurance, Employees Provident Fund and personal savings. The retired saved an average of RM478 a month, and the working RM704, figures that were considered low compared with other countries. Malaysian retirees feel that their retirement income is insufficient to cover household expenses. Their average income is RM1,243 but the amount they need is RM1,568 a deficit of RM325, she said. In comparison, Singapores average retirement income is RM3,690, and the amount needed RM3,465; while Thailands average income is RM1,276, and the amount needed RM903, according to the survey. The disparity between high and low income earners in Malaysia is wide, the high-income retirees having four times more than those with low income, the survey found. Despite insufficient income, three-quarters of the retirees said their quality of life had improved if not remaining the same, while 83% of the working group expect their quality of life to improve or remain the same. Jika diamati artikel diatas memang menakutkan.Persoalannya sekarang adakah simpanan kita mencukupi setelah kita bersara nanti atau kita masih lagi perlu bekerja untuk menampung kehidupan selepas bersara??? Tahniah kepada yang telah bersedia dan kepada yang belum bertindak saya nasihatkan bertindaklah sekarang sebelum terlambat. Masa begitu cepat berlalu.. Ingin Maklumat lanjut atau ada sebarang pertanyaan tentang perancangan hari tua anda atau pelaburan bersama Public Mutual boleh PM saya.Boleh juga sama2 berkongsi pendapat di sini semoga menjadi panduan buat kita semua. -------------------- Agency Manager, Public Mutual

019-6928364 @ nazri.amirul@gmail.com ym; amirul.nazri |

|

|

|

|

Apr 13 2009, 12:45 AM

Kiriman

#12

|

|

Eksekutif Junior Kumpulan: Member Rasmi Kiriman: 439 Sertai: 8-April 09 Daripada: Taman Equine/keramat/pchong No. Ahli: 855 |

kalau org yg gaji kecik < 1k..leh ke nak melabur ni?

pastu..minima pelaburan brapa? -------------------- |

|

|

|

|

Apr 13 2009, 03:08 PM

Kiriman

#13

|

|

|

Bukan Eksekutif Kumpulan: Member Rasmi Kiriman: 12 Sertai: 12-February 09 No. Ahli: 689 |

QUOTE (bizonedrop @ Apr 13 2009, 12:45 AM) kalau org yg gaji kecik < 1k..leh ke nak melabur ni? pastu..minima pelaburan brapa? boleh. sbb syarat wajib hanya Minimum pelaburan RM 1K, regardless gaji anda less than 1K.

-------------------- Agency Manager, Public Mutual

019-6928364 @ nazri.amirul@gmail.com ym; amirul.nazri |

|

|

|

|

Apr 13 2009, 03:09 PM

Kiriman

#14

|

|

|

Bukan Eksekutif Kumpulan: Member Rasmi Kiriman: 12 Sertai: 12-February 09 No. Ahli: 689 |

Start Buying Now. Seriously.

iFAST Corporation co-founder and executive director Moh Hon Meng says its time to go back into equity markets. So have investment legends like Warren Buffett, who bought in October, John Bogle, who said in this month that equity markets are too low and Bill Miller, who recently said that he sees great value in equities. (I am nowhere near an investment legend, but I am following their lead). This is opposed to the doomsayers who say that the worst is yet to come. These doomsayers are who are they again? Its interesting for me that there are always investment experts who criticise Warren Buffett. They say he was irrelevant to the new economy in 1999, when he refused to buy technology shares. They say he didnt understand the situation when he said that financial derivatives were financial weapons of mass destruction back in 2002. And now they say that he is simply trying to talk up his own investments, when he said recently to Buy America. These things they say of the worlds most successful investor, the worlds richest man. Nobody remembers these they, but Warren Buffet continues to make loads of money from his investments. Lets look at the reasons why they say things will get worse. This time its different Youve heard this one. They say this time its different because its an unprecedented global economic slowdown not seen since the Great Depression. To this I have two responses: Its always different. If it wasnt different, no one would panic, and no one would sell their shares, and stock markets wouldnt fall. For example, if a plane slams into a major building somewhere tomorrow, (it would be a tragedy, but) world stock markets would not crash the way it did in the aftermath of September 11th. The Asian financial crisis, tech bubble bursting, Iraq and Afghanistan wars, SARS, sub-prime crisis, they were all different. Its never different. What doesnt change is that the human race has always been able to find solutions to these problems and emerge stronger. This is a unique trait that human beings have. If we did not have this trait, we wouldnt have evolved as a species. This is one of the reasons world stock markets grow over the long term; we always grow and thrive as a species, and we always find solutions to problems. We dont have clear signs yet that a recovery is in sight This is what many analysts say. Again, I have two responses: If we had clear signs, the stock markets would have gone up a lot, and you would have missed the opportunity to make inordinate profits. Stock markets always anticipate economic recoveries. By the time the analysts are able to report clear signs, we would be more than halfway to the top. We do have some clear signs of action. We know that these actions are being taken. Monetary policy actions: We have seen governments across the globe cut interest rates and increase money supply. In recent weeks, we have announcements coming out of the U.S., the E.U., the U.K, Australia, China, Korea and others. These are extremely expansionary. Fiscal policy actions: More and more governments are injecting billions into their economies. Usually they will do this by funding infrastructure projects, reducing taxes, and so on. This will increase overall demand and stimulate the economy. In a short time, the global economy will feel the effects of these actions. So yes, we do have a recession. But a lot of smart people at governments all over the world are working frantically to address it. The fiscal policy actions are easy to understand, but if you always wondered why interest rates have such a big impact, the reason is this: private companies always have expansion plans. They may be reluctant to borrow funds to expand if borrowing costs are high. They will be particularly cautious in a recessionary environment. But when rates decline, many will start borrowing, start hiring and start expanding. The recession will extend for another 3 quarters This seems to be the consensus economic forecasts. But lets say this is true. Three quarters means the last quarter of 08 and the first two quarters of 09. Lets budget another quarter and say it goes on till the end of 3Q 09. I dont want to forecast when the economy or the stock markets will recover. But I can say this: the stock markets always recover before the economy does. Conclusion Has the market reached a bottom? I feel strongly that either: We have passed it. October could have been the bottom. We are very near it. A lot of the bad news has been priced in. Given the very low valuations now, theres not much downside, which makes the upside over the next two years very interesting. Do not punt. Make sure you invest with money you can set aside for at least three years. This is because: You dont want to be caught having to sell at the wrong time. You need time for the markets to realise its full recovery potential. This is the time to invest profitably. Seriously. -------------------- Agency Manager, Public Mutual

019-6928364 @ nazri.amirul@gmail.com ym; amirul.nazri |

|

|

|

|

1 pengguna membaca topik ini (1 Tetamu dan 0 Pengguna tidak dikenali)

0 Ahli:

| Versi Ringkas | Masa sekarang: 27th April 2024 - 10:52 PM |

Powered By IP.Board

2.3.3 © 2024 IPS, Inc.